03.02.11

How to Build a Bad Bank—for the Greater Good

Among the many unwanted things that taxpayers get socked with during a financial crisis is a portfolio of deeply distressed assets—loans gone sour, millions of them, many of them sliced and bundled into securities that nobody can sell because nobody wants to buy. The overwhelming uncertainty around these troubled assets can paralyze the financial system. Almost inevitably, they fall into the government’s hands as a side effect of efforts to rehabilitate the financial system and restore credit flows.

It’s an important and necessary step in nursing the financial market back to health. The government usually takes possession of troubled assets either through receivership of failing financial institutions or through programs that strip distressed assets from struggling but still open-andoperating financial firms.1

These assets often go by the infamous term “toxic assets,” the likes of which throttled so many financial institutions in 2008 and 2009. And despite the economic damage they did over the past few years, the problem of what to do about them persists. Elements of the Dodd-Frank legislation go a long way toward averting and dealing with financial market meltdowns, as the legislation establishes a separate Federal Deposit Insurance Corporation (FDIC) resolution authority for nonbank financial firms. But absent from this legislation are provisions for handling troubled assets on the scale generated during a financial meltdown.

It is true that the FDIC’s receivership operations are set up to dispose of the assets from the estates of failed financial firms during non-crisis times. U.S. federal deposit agencies are funded by assessments on the industries they insure, which limits their resources for dealing with largescale banking problems.

In other words, the FDIC’s operations currently are not geared toward dealing with the volume of distressed assets that would likely need to be managed in the aftermath of a financial crisis; systemic crises require the marshalling of resources beyond those normally available to the deposit guarantor. Hence, there is a need for an institution whose sole purpose is large-scale asset salvage—to acquire, manage, and then dispose of the overhang of distressed assets on the books of banks and other financial firms.

Such an institution is not a new concept. The government and even the private sector have created special-purpose entities to deal with troubled assets in all of the recent financial crises. From the Great Depression to the 1980s savings and loan debacle, vehicles of this sort have played a role in getting the financial market functioning again. Some have done their jobs quite well; others not.

Drawing on these lessons, I propose the creation of a resolution management corporation, or RMC. Call it an asset-salvage entity, or bad bank. The RMC that I propose would be sponsored by and operated by the federal government. It would become operational only in response to a financial crisis where the volume of troubled assets that needs to be managed and disposed of exceeds the capacity of the FDIC’s receivership operations.

The RMC’s overarching goal: restoration of a stable, healthy financial system at a minimal cost.

The Trouble with Assets

An asset is said to be troubled, toxic, impaired—pick your term—under a number of different conditions. If it is a mortgage loan, it may be “nonperforming,” that is, the borrower is no longer making payments. It could be an entire bundle of mortgages made to subprime borrowers, in which case finding a market value may be impossible.

It’s like a carton of eggs in a supermarket. They might appear to be fine eggs, but if shoppers suspect they might be tainted on the inside, the eggs might not sell at any price. The market reaction to toxic assets is much the same.

These toxic assets, if large enough in scale, could wreak havoc on the economy. Financial institutions are reluctant to sell them, because the markets for these assets, if working at all, tend to be very thin. The problem is made worse if financial firms holding the assets are undercapitalized and likely reluctant to undertake any actions that would require them to recognize losses on these assets. Creditors and counterparties grow nervous about doing business with toxic-asset-owning financial institutions. Over time, the uncertainty bleeds out into the real economy, freezing the fundamental financial-sector activities of facilitating people’s and firms’ borrowing, saving, and investing.

The logic of stripping away toxic assets from their current owners is the same as ripping off a bandage—it hurts, but it’s best to get it over with quickly. Otherwise, you only prolong the pain.

History clearly teaches us the downside of nursing along struggling firms—from the savings and loan industry in the 1980s to Japan’s banks in the 1990s. Instead of shutting them down and seizing their assets, the government injected these firms with liquidity and capital, further exacerbating and extending the economic decline. By one study (DeGennaro and Thomson), regulatory forbearance—a policy of delaying a receivership process—quadrupled the cost of the savings and loan crisis for taxpayers.

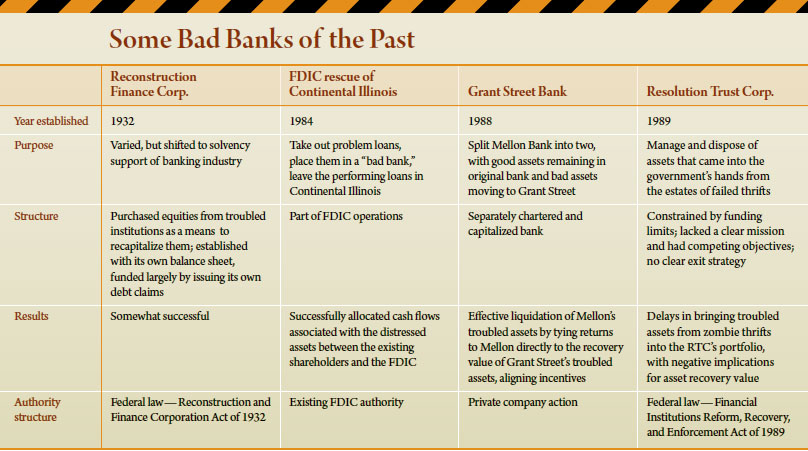

Until now, the way the government has gone about trying to restore order hasn’t been very systematic. Past experience with bad banks is mixed. The Federal Deposit Insurance Corporation had some success in setting up a bad bank to handle the rescue of Continental Illinois Bank and Trust Company of Chicago in May 1984; the 1989-created Resolution Trust Corporation, by contrast, was hobbled for various reasons in its ability to manage assets from failed thrift institutions (see box: Some Bad Banks of the Past).

Four Keys

So, how should we go about establishing an effective bad bank? Four features are crucial to the proper design of my proposed resolution management corporation:

1. Transparency and accountability

Taxpayers need to be able to track losses and gains. This can be accomplished by a crystal-clear separation between the “good” and "bad" assets, acknowledging at the start the losses from toxic assets and the costs associated with managing and disposing of them. This allows for an auditable allocation of losses, which in turn properly aligns incentives for efficient management and disposition of the toxic assets.

The more transparent decisions are at the beginning, the more likely it will be that the financial system can be rehabilitated quickly and credit flows restored. A straight-forward way to accomplish a transparent separation of toxic assets from the financial system would be to put the failing institution through a receivership process.

A systemic regulator—perhaps the Board of Governors of the Federal Reserve System along with either the FDIC, the SEC (for securities broker-dealers), or the Federal Insurance Office (for insurance companies), in consultation with the Secretary of the Treasury—would make the call on which firms should pass into receivership.

The troubled assets—mortgage securities and so forth—would be set in a pile and valued as fairly as possible (which, granted, could prove difficult). The creditors might receive a certificate with a percentage claim to any future cash flows from the asset. There might even be a certain comfort level in handing over the assets because of the next stage of the process.

2. A simple, unambiguous mission

A resolution management corporation should aim to maximize net recoveries on the portfolio of distressed assets under its management. Period.

The bad bank must quickly return assets to the private sector at the highest possible recovery value. A fast realization of losses is the surest path to economic recovery, as financial market players can effectively take their lumps and move on. The sick institutions themselves could be passed into a bridge institution where they would be recapitalized, and the bad assets moved into the resolution management corporation for management and rehabilitation.

If it’s a security with, say, parts of 1,000 subprime mortgages, there may be no initial market in which to sell it. So the RMC would hold the security, and perhaps even take the time and effort to “rehabilitate” some of its underlying mortgages. Perhaps a certain homeowner had been out of work and not paying, but then found a job. The RMC could conceivably be the one that makes the phone calls to get the borrower back on a payment schedule, even if at a reduced rate.

There must be confidence that the bad bank will care for the assets and then speedily return them to the private sector, or be held responsible if not. The Government Accountability Office should conduct periodic audits; Congress should hear regular testimony from the bad bank’s chief; and Congress should establish an independent body to oversee the operations and activities.

3. Adequate resources

Bad banks need funding and staffing. The funding is to pay for operations and costs associated with stripping troubled assets from the failing institution.

The independent bad bank should be given a revolving line of credit with the U.S. Treasury, enough to fund operations during the start-up period—perhaps about $100 billion.

In this initial phase, the bad bank can acquire assets in a manner that preserves their value and reduces losses that insolvent and possibly neglectful institutions had let mount. After that, the bad bank should seek permanent operational funding from direct Congressional appropriations and issuance of bonds. The principal and interest on the bonds would be funded through the (eventual) liquidation of the assets. Because assets should be acquired at fair value, little or no additional funding should be required to cover shortfalls in the value of assets sold.

However structured, a bad bank should essentially be established as a shelf organization. Its charter, funding authority, and authorization for staffing and other resources would always be in place, but the RMC itself would be dormant until activated. And that activation should happen only in case of a real fire—a widespread financial crisis, not the sort of higher-frequency disruptions that are normal in a cycle. Who would declare the RMC’s activation is a matter of preference—it could be the FDIC’s board, the newly created Financial Stability Oversight Council, the Board of Governors of the Federal Reserve System, the Secretary of the Treasury, or some combination of these.

4. A limited life span

Once the troubled assets have been repaired and re-sold, the bad bank can fold up.

Establishing a fixed expiration date clearly ties the existence of the RMC to its function. Ten years seems like a reasonable maximum life for such an entity. Once the need for the function goes away, the RMC does, too. It also reduces incentives to speculate on asset-recovery values by limiting the maximum time any asset can be held. There is also the more technical but important benefit of easing uncertainty among market players about who will issue claims against the expected cash flows from the troubled assets. They will have a rough idea when the cash will start flowing, because they know the bad bank will cease to exist when its job is done. Any assets remaining on the RMC’s books when its charter expires could be turned over to the FDIC’s receivership function for eventual sale or liquidation.

A Necessary Reform

The way we respond to crises can either help or hinder the recovery. The establishment of a government-chartered RMC could go a long way along the “helping” path. At best, a national “bad bank” should be seen as a complement to other financial-crisis rescue efforts. We will still need emergency liquidity and credit programs, for example. But financial crises have grown more frequent in recent decades. Perhaps if we had a system for dealing with the most troubled assets up front, we would lessen the need to deal with another crisis in the near future.

Readings

- DeGennaro, Ramon P., and James B. Thomson. 1996. “Capital Forbearance and Thrifts: Examining the Costs of Regulatory Gambling.” Journal of Financial Services Research 10(3): 199-211.